A few weeks ago I reflected on the psychological drivers behind referrals: why a genuinely satisfied client so often says and does nothing, and what that silence turns out to mean.

Since then I have been listening back through the Financial Planner Life podcast,1 where a guest made an observation worth pausing over. Referrals, he said, are difficult to scale, not least because there are only so many people any client actually knows.

It is an interesting paradox. Some advisers swear by referrals as their primary growth engine. I know of one US-based firm that grows by almost nothing else. And yet the actual number of referrals being made runs well short of what advisers expect once a client relationship is strong and long-standing.2 Evolutionary psychology and anthropology have an answer for the gap, and it is a specific one: something known as the Dunbar number.

The Dunbar number

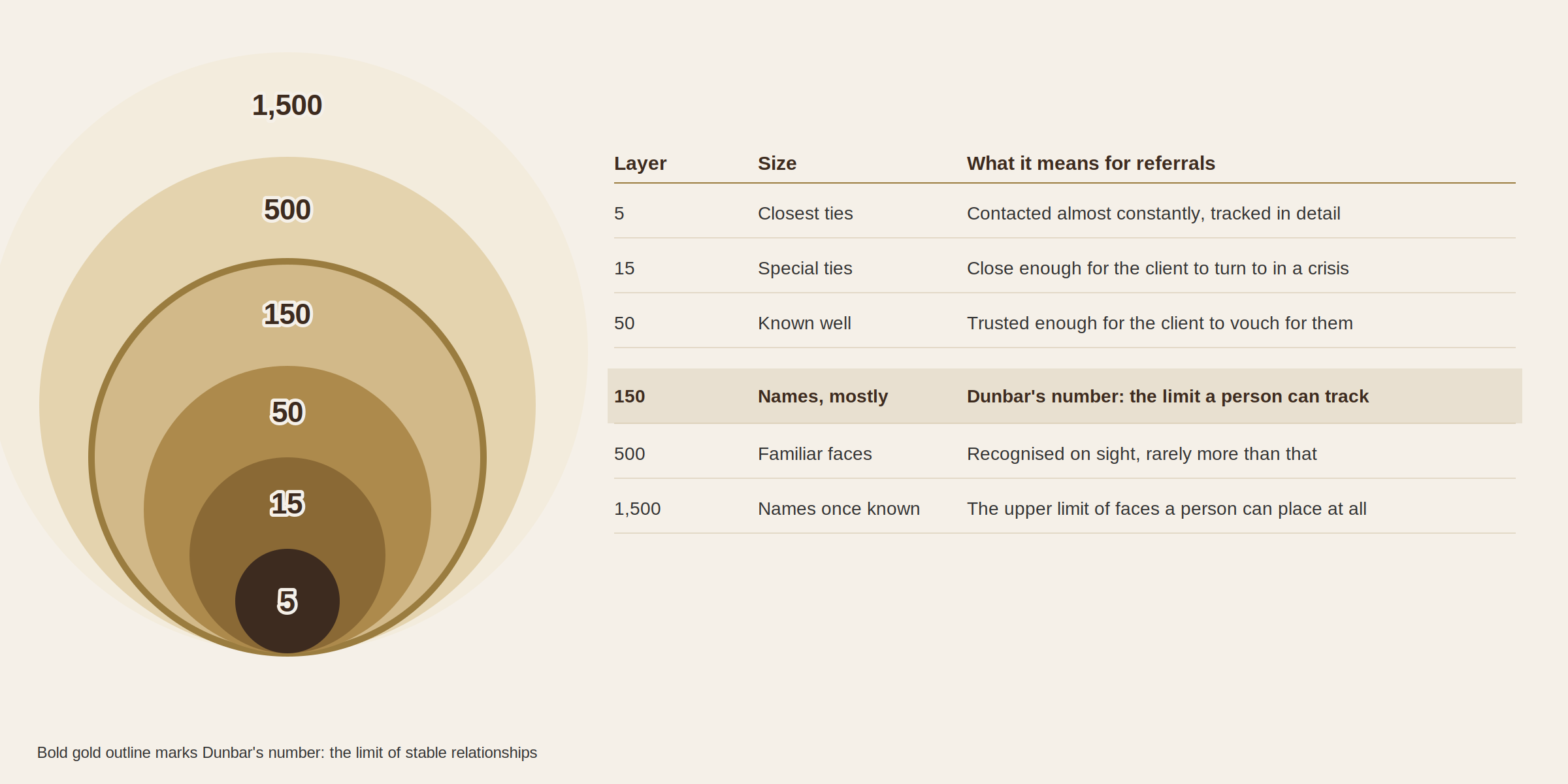

Robin Dunbar, an anthropologist and evolutionary psychologist at Oxford University, spent years studying the relationship between brain size and group size in primates, humans included. His finding was that the capacity to track relationships, to know who someone is, what they are dealing with and whether one's own reputation is safe in vouching for them, is cognitively expensive, and that expense sets a hard limit on how many people a person can hold in mind at once.3

That limit is not one number but several, arranged in layers like an onion, each roughly three times the size of the one inside it.4 At the centre sit around five people: the ones contacted almost constantly, whose lives a person tracks in detail. Around them sit a further ten to fifteen, close enough to turn to in a crisis but not part of daily life. Beyond that, a band of around fifty, people invited to a significant gathering. The outermost of the well-known layers is the 150 itself, popularly called Dunbar's number, the point past which a person cannot keep track of who someone is and how the two of them relate, only that they exist. Two further layers sit beyond it, a 500 of somewhat familiar faces and an outer 1,500 marking the limit of names a person can place at all, but neither carries much weight for referrals.

The inner layers matter more than the headline figure. Referring someone is an act of vouching, and vouching draws on trust that only the inner layers hold in any depth. A client's outer 150 is mostly names, not people they would stake their own standing on introducing. The genuinely referable slice of the network sits far closer to the centre, in the fifty or so people a client actually knows well, and within that fifty, only a handful are likely to be at a life stage where a financial planner is relevant at any given moment. That narrowing, layer by layer, is what the podcast guest was pointing at, and it is why the real number of referrals a satisfied client can generate over a relationship's lifetime is smaller than a simple headcount of their acquaintances would suggest.

A client's silence usually has a reputational cause: they stay quiet because vouching puts their own standing at risk, and lowering that risk is real work worth doing. A second limit sits beneath it, and no amount of reassurance moves this one. Even a client with total confidence can only draw on the fifty or so people they track well, and the relevant slice of that fifty is small at any given moment.

What this means in practice

The two limits call for different responses, and treating them as one is where most referral programmes stall. Lowering reputational risk converts more of the willing fifty into actual introductions. It cannot make the fifty bigger. Growth beyond that ceiling needs a second lever, not a harder pull on the first.

- Notice whose fifty already sits near transition. Accountants, solicitors and similar professions place people in front of change as part of the job, which means more of their network is relevant at any given moment than an equally warm client in a quieter line of work. A simple occupation tag in the CRM is usually enough to see who qualifies.

- Expect a client's fifty to resemble the client. Homophily, the well-documented tendency of people to cluster with others like themselves, means a newly retired client disproportionately knows other people newly retired.6 The relevant slice of a client's network is not a random draw. It looks like the client sitting across the table.

- Let the client's own experience shape the ask. Rather than a general prompt to think of anyone who might benefit, a reference to what the client has just been through does the work homophily predicts it will. A client who has just sold a business is more likely to know someone else mid-sale than a stranger picked at random from their fifty, and naming that specific situation is easier to answer than an open one.

The ceiling is real, and accepting it is more useful than arguing with it. A client's fifty was never going to carry a practice's growth by itself, however well the reputational risk is managed, because no amount of trust changes how many people a person can actually track. What changes is knowing where to look next.

The clients whose networks sit closest to transition carry more of the opportunity than an equally warm client in a quieter life, and the client's own recent experience, named specifically rather than gestured at generally, does more work than any script ever did.

Put together, that is not a smaller version of the old approach. It is a second, genuinely scalable stream sitting alongside the first, and a practice that builds toward both is in a stronger position than one still hoping a single client's fifty will stretch to cover the rest.