When markets correct, clients who appeared content and committed suddenly want to act, and acting usually means selling into the fall, pausing contributions or shelving decisions already made.

As reliably as the sell-off itself, 'help' arrives from the large institutional players, vested interest packaged as reassurance: the chart of past crises survived, the laundry list of cognitive biases and the talking points for the next call. Underneath sits a single assumption and the instruction that follows: that the client is 'irrational' and should stay the course, that 'historically markets always recovered', and that 'you'd not want to miss the ten best days'.

The instruction is sound as far as it goes. The statistical case for staying invested is sound, and these tools make it cleanly. It also reassures almost everyone except the person it is aimed at because it answers a question about aggregates while ignoring the one being asked: 'what does this mean for me, specifically?' This space between the two is where the reassurance tends to fail and financial plans begin to unravel.

This reflex, to recycle the familiar kit, to educate and explain, is rarely the planner's fault. It is a legacy of the industry's comfort zone: cast client behaviour, and often human behaviour at large, as irrational, then correct the irrationality with 'rational' charts and expert guidance. The story repeats, as cyclical as the markets themselves.

There's a better way, though, and it starts by taking the client's apparent irrationality seriously enough to see it is not irrational at all.

The average is not the client

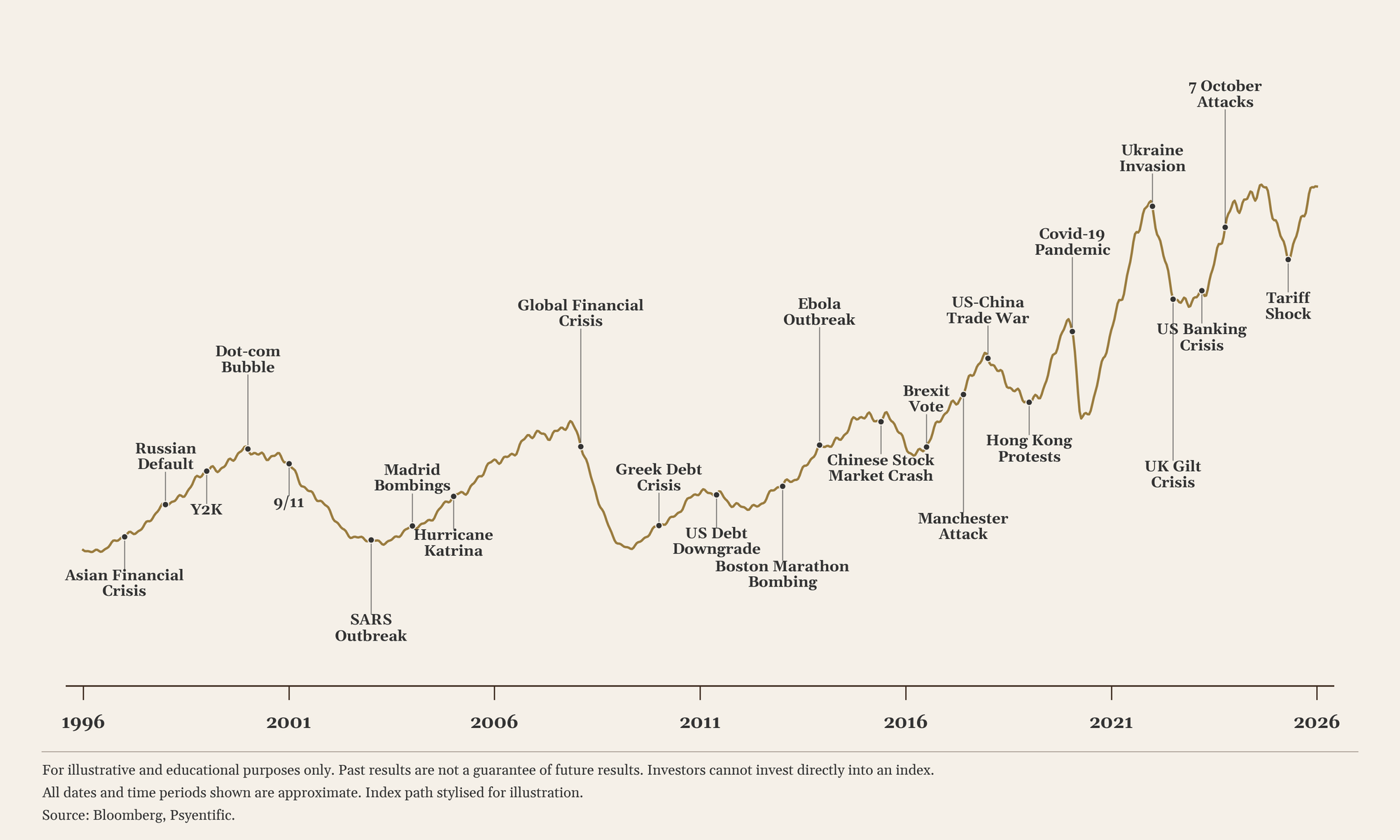

The asset I see most often, and the one asset managers are keenest to supply, is a version of what gets called the Wall of Worry: an index, usually S&P 500, plotted from inception, every crisis it has weathered flagged along the climb. A monument to the resilience of markets, and to the capitalism that, as UBS Global Wealth Report reminds us, has made us so much wealthier.1

Factually, the chart is impeccable. It is also the one clients seem to care about least. As one savvy UK financial planner put it to me, 'most wealthy clients have already seen a version of it'.

The chart is meant to make recovery easy to picture and 'staying the course' seem like a no-brainer. Familiarity wears the message smooth.

That is half the problem. The other half is the language the industry has been conditioned to deploy:

- 'On average...'

- 'Historically, markets...'

- 'The probability of...'

- 'Over the long run...'

- 'Most investors who stayed the course...'

The client asks about themselves. The phrase answers about everyone. What should be an intimate conversation about one person's money turns into a recital of the industry's stock vocabulary. Mathematics and behavioural science both explain why the result lands so far from the intention.

The error in the maths

There's a concept known as ergodicity. It sounds forbidding and turns out to be simple. A process is ergodic when one path followed for a long time behaves like many paths averaged at a moment.2 Time and crowd give the same answer.

Picture a thousand people in a casino for one evening. A handful win big, most lose a little, and the house takes its expected cut from the room as a whole. That is the ensemble: the average across everybody. Now follow one of those people, the same odds, every evening for a year. The room's tidy average says little about that one person's year, because somewhere in it sits a night that clears them out, and a player who is cleared out does not play on.

That gap, between what is true of everyone at once and what happens to one person over time, is where the trouble lives. The casino is ergodic enough. The player is not, because ruin is final for them and not for the room.

Markets sit closer to the casino than to the player, though not in the way that first sounds. The parallel is not the odds; markets, unlike the table, tend to pay the patient investor over time. The parallel is finality. Pooled across enough investors and decades, the index has no mortgage, no redundancy, no retirement date and no nerve to lose. Nothing that happens to it is final. It has the time to wait out any drawdown, and the indices we still quote are the ones that did.

The client is the player's case. They live one path, in one order, with hard stops the index never meets: the forced sale in redundancy, the drawdown that cannot wait, the year the income has to start. 'Markets tend to recover' is true of a thing that cannot be ruined, said to a person who can.

None of this makes the chart wrong. The average is real, the recovery did happen, and that is exactly the trap: a true answer to a question the client did not ask.

That is the mathematics of it. The behavioural science is worse, because a true answer landing on the wrong question does not simply miss. It can cost you the client.

The error in the room

Picture the client who is actually frightened. They are not asking how markets behave. They are asking whether their own plan, their own retirement, survives this. A fact about everyone slides straight past that, and they know it has, even if they could not tell you why.

There is a label for it, of course. Egocentric bias: caring more about your own situation than the wider view seems to merit3. The industry inherited the term and mislaid the nuance, filing it under things to correct swiftly. Usually reasonable. Not here. A person fixed on their own single life is fixed on the only one that can actually happen to them, which is less a distortion than plain good sense.

Which is why the chart does not just miss. It can sting. Someone has brought you a private fear and you have handed back a population. The maths is sound and the gesture is cold, and it is the coldness that lands. Underneath it sits a verdict the client hears even when nobody means to send it: your fear is a failure of perspective, and here is the data to correct you.

The way I put it to advisers is this. Your child comes home in tears because someone called them stupid. You do not reach for national percentile data on childhood IQ. You do not defend the average at the kitchen table. You attend to the one child in front of you, because the average was never the thing that hurt. 'Markets always recover', produced to a client who is afraid, is that percentile chart, slid across the table at the worst possible moment.

A client who feels unheard does not settle. They press harder, book another call, move a slice to cash where the number at least stops falling, shelve the contribution that was the whole point of the plan. The reassurance meant to calm them has done the opposite.

None of which is an argument against knowing the numbers. The numbers are the easy part, and most advisers have them cold. The harder part is resisting the reflex to lead with them, and that is where the better conversation begins.

A better conversation

What replaces the chart is not another chart. It is a sequence, and it runs in the order a frightened call actually unfolds: hear the client, locate the real risk, settle the response in advance. None of it needs new tools, only the discipline to hold the reassurance back until the first two are done.

Step 1: Name the real fear

Before any data, say back what the client is really feeling, even when they cannot fully put it into words: 'It sounds like the real worry is whether your plan holds if this one takes years to come back.' Reflecting a concern back tends to lower a client's defensiveness rather than raise it4, and putting an emotion into words has been shown to reduce its intensity.5

Delivery matters as much as the words. Tone and form do the work: a question rises at the end and reads as a test, a statement falls and reads as understanding. 'Are you worried this won't recover in time?' invites the client to defend their panic. 'You're worried this won't recover in time' tells them they have been understood. The shift from question to statement is small and genuinely hard to hold under pressure, where the reflex is to ask and to fix.

Done well, this is the move that earns everything that follows. The client who feels heard stops bracing and starts listening. Skip it, and every sensible thing said next arrives as noise, because the person it is aimed at has not yet been reached.

Step 2: Map the fear onto their life

The fear has a name now. Next it needs a map. The recovery only matters to a client still invested when it arrives, and what keeps them invested is rarely the return itself. It is the goal underneath it, the thing the money was always for. So the work is to find the points where this particular life could force a sale at the wrong moment, and deal with each one before it does.

Take them in turn. Is there income that might stop, through redundancy or a business going quiet, and how long could the gap run before investments have to be sold to cover it? Is there a planned withdrawal, a house purchase, a tax bill, a child's fees, that lands on a fixed date regardless of where the market is that month? Does the cash buffer genuinely cover those calls, or only the comfortable ones?

Each has a practical answer, and each answer makes the fear smaller by making it concrete. The conversation is now about this client's life, not the market's history, which is the only place the fear was ever going to be settled.

Step 3: Pre-commit the response

The last move borrows from what behavioural scientists call the implementation intention, or if-then plan: deciding the specific response to a situation before it arrives makes the intended action far likelier to survive the moment.6

Settle, in writing, what happens if the portfolio falls another five, ten or fifteen per cent. What gets sold and what gets held, depending on whether the fundamentals have actually changed. What gets bought, because a fall is also when things go on sale. And who calls whom when it happens, which, for the avoidance of doubt, is the adviser.

The next correction

Markets will correct again, and the calls will come again — inevitably. The reflex to reach for the chart will be as strong as ever, and the chart will be as true as ever. What changes is who the answer is for. Aimed at the average, it reassures no one in the room. Aimed at the client, the same care turns a falling number into a plan they helped build.

None of this is softer than the old approach. It is harder, and it is the actual job: making one plan survive contact with one life. The apparent irrationality the industry sets out to correct was sound judgement all along, and the work is not to talk the client out of it but to plan around it. That shift is subtle, rarely credited, and most of what a good financial planner is actually for.